Emerging Markets will Fail to Navigate Automation + Carbon Reduction. Here’s why…

I wrote this essay on May 12, 2021 as part of Write of Passage, an online writing course.

Emissions Standards + Automation = Major Threat for Emerging Markets

Automation and the cost of stringent emission standards will hurt emerging markets (EMs) much more than is generally appreciated, and the pain is likely to become pronounced this decade.

Media coverage about carbon taxes and automation (including robots) is biased towards developed markets. However, it is actually emerging markets that will endure a much more painful transition as direct and indirect carbon taxes and low-cost automation encroach into day-to-day life. The pain on emerging markets will be immense, and will eventually ricochet on developed markets, which is why it behooves everyone to think about how EMs will weather these typhoons.

I’m writing this article not because I’m against lower emissions, automation, or international agreements. In fact I enthusiastically support all of these. I hate air and water pollution and wish more was done to address these concerns. I grew up in Mexico City and as an adult have mostly lived in Hong Kong. Both are terrible cities when it comes to pollution, and both with inept leadership lacking any sense of urgency on these issues. I also don’t dispute a need for urgency; many of the most tragic climate event risks are likely to impact emerging markets, who are the least capable of paying for the recovery.

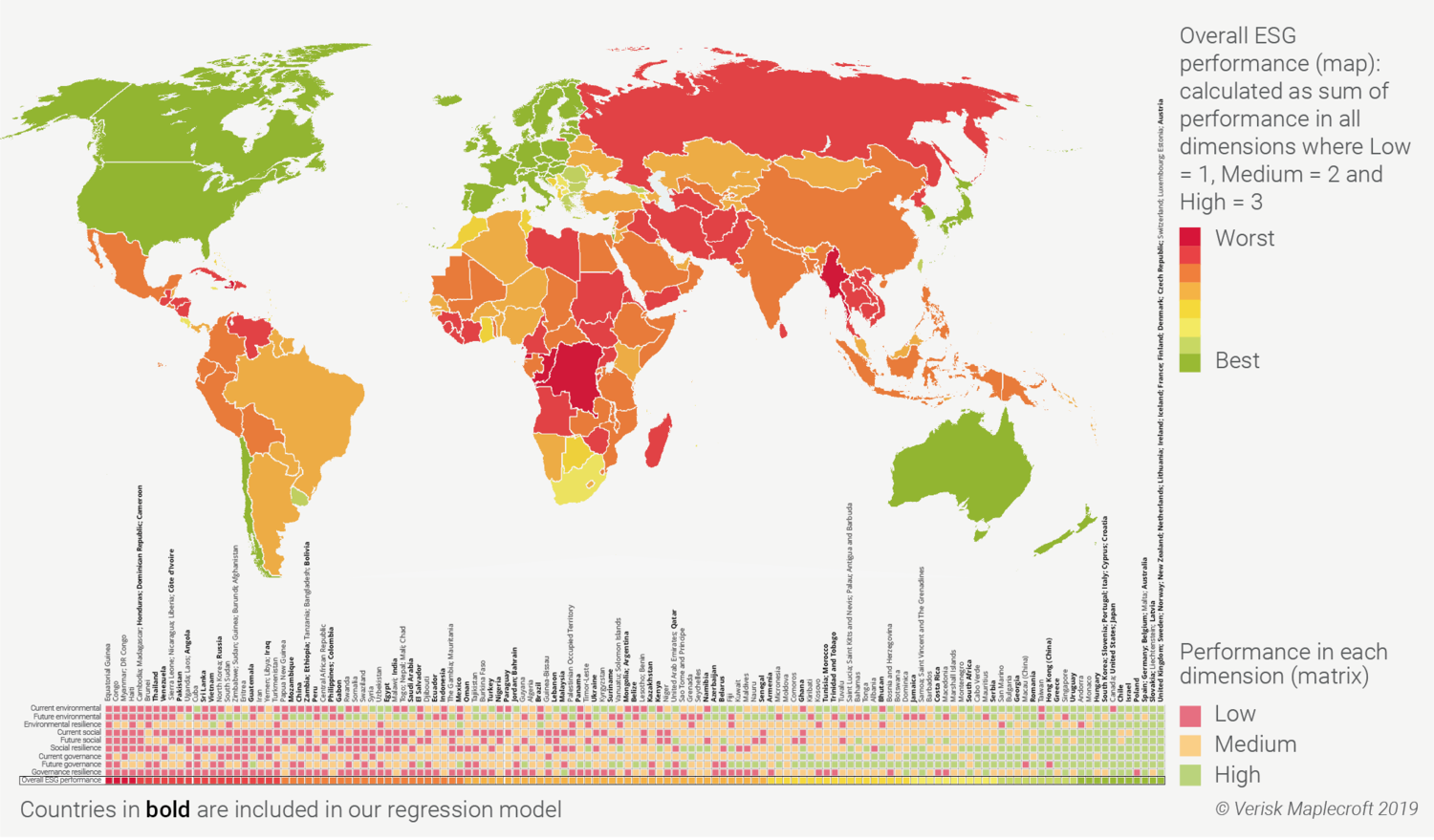

For a visual of who will benefit the most from improved adoption of environmental standards, the following map is a great primer. However, instead of reading the color codes as an indicator of emissions compliance, think of the colors as indicators of probable future GDP growth in a decade of aggressively targeting lower emissions.

Green = Go; Orange = Slow-Down; Red = Stop (or reverse).

Most of the world lives in the red and orange countries. The green countries + China drive most international policy targets and also control the purse-strings of investment capital. Just as globalization was catalyzed by the off-shoring of polluting and dangerous industries, developed countries have decided now is the time to reverse this trend.

Aggressive lower emission targets + automation = anti-globalization?

The irony is that although most of the accumulated pollution in our planet comes from developed countries, emerging markets are today relatively more reliant on coal-fired power, making their adjustment all the more difficult. The cost of switching to less polluting power sources is more expensive for EMs, not just because they often pay a higher cost of capital for project finance, but also because the cost of developing all the associated infrastructure for other fuel sources tends to be much higher. While international agreements have provided explicit concessions to EMs, these same countries are already experiencing indirect shadow ‘taxes’ in the form of developed market capital providers becoming increasingly reluctant due to activist pressure to finance anything that has high carbon emissions.

Something about this noble environmental movement seems to be neglecting the complex economic and social impacts on emerging markets.

Why now?

The carbon reduction movement has reached a tipping point. It’s no longer a check-the-box side-show for providers of debt or equity, but rather a critical part of the investment-memo. COVID seems to have dramatically invigorated this movement. Also, markets that trade in carbon credits are working, creating a mechanism to tax pollution. Europe is at the forefront of adding carbon taxes to goods imported from jurisdictions that don’t tax pollution.

Traditionally passive ‘long only’ equity investors have become quiet activists. Banks and credit funds have started to shun energy intensive borrowers who principally source their energy from coal-fired power plants. This effectively becomes an indirect tax to the borrowers making the cost of projects more expensive, potentially to the benefit of projects in developed markets that have access to cleaner fuel sources.

For example, a recent investment-grade $300 million bond issuance by an Indonesian nickel producer recently failed to meet its funding target because many investors now have restrictions on investing in energy-intensive businesses that use coal power. Indonesia as a country is almost entirely reliant on coal-fired power and this is something that sovereign investors are increasingly starting to scrutinize. Less capital availability simply means you have to pay more to attract other investors.

Switching now to the impact of automation on emerging markets: Every generation of robots delivers increasing productivity at a declining cost - a dynamic that no labor pool can match. China is doing to entry-level robots what it has done to consumer electronics for the last 40 years: produce a quality product at high volume and low cost. Robots that have so far mostly been a developed market phenomenon have started to enter the factory floor of emerging markets. No visas, contracts or labor unions to contend with. Employers will be spared the headaches and risks that come with large labor pools, but in exchange will contribute to social problems as no new industry will develop fast enough to absorb all of the redundant labor.

The table below shows the rapidly declining cost of robots. The “Payback Period” (cost vs. human labor) is rapidly declining.

Source: FT.com, June 6, 2016, China’s Robot Revolution

The following tables show the dramatic uptake in robot usage as the price falls...

The following table shows data for jobs that have been particularly impacted by automation in a US context. As the cost of automation declines and they are introduced to emerging countries, the impact to EM will be far greater because of the larger percentage of the population working in these types of jobs. Highlights are for those sectors particularly relevant to many EMs.

The following table shows expected in-roads of automation across many sectors. There is no sector that is not impacted by robotics.

Who is Going to Pay?

The challenges of aggressive emissions targets and automation to emerging markets are not being adequately studied. How much will it cost to retrain and provide long-term subsidies potentially to 10, 20 or 30% of the working population replaced by automation? How much will it cost to transition to non-coal sources of power? In the meantime, what will the “carbon-premium” be that these countries need to pay to access foreign capital markets?

Most importantly, who will pay for it? It will be extremely difficult for EMs to internally fund this transition. Unfortunately, developed countries offer little hope. Europe and the US are more inward focused today than they have been anytime since WW II, and partly for good reason; these countries have massive underfunded pensions, excessive government debt and an increasingly unhappy middle-class. Europe and now the US are embracing carbon reduction and automation because they are in a position to be economic beneficiaries of these trends.

Will rich countries be able to subsidize poorer countries with their gains from carbon policies and robotics? I doubt it, but I do see two scenarios where they may act meaningfully:

One is if the impact to emerging markets is so devastating that it poses security risks domestically or to trade routes;

Another is if China and the West find themselves competing in a new “Great Game” to win influence in emerging markets.

The tremendous accomplishments of development achieved in Taiwan, Korea and China serve as inspiration for what could be possible for other emerging countries, although it is hard to imagine any large EM such as Indonesia or Vietnam becoming high income countries in our lifetime. Education standards tend to be low and there tend to be many social and political impediments to mobility for ambitious individuals, notwithstanding the tremendous hope offered by the internet. Furthermore, carbon reduction targets and automation turn my skepticism of continued EM wealth creation into a conviction that this trend will stall and even possibly reverse in the coming decade. I’ll be reading and writing more about this, and I’m keen to have my convictions challenged - fodder for future essays...